The Growing Tax Squeeze on Wealthy Homeowners

June 10, 2026

Marilyn J. Gentilotti, Esq., CPA, CFP®, CTFA, AEP®

Vice President and Senior Wealth Planner

Washington Trust Wealth Management

If you own a second home, rent out a vacation property, or are planning a high-value real estate transaction, you may have noticed a growing trend: states and municipalities are increasingly looking to affluent homeowners, investors, and luxury property owners to help fund housing initiatives and close budget gaps.

The newest example is Rhode Island’s widely discussed “Taylor Swift Tax,” but it is far from the only effort aimed at higher-income households or high-value property. Across the Northeast, policymakers are rolling out taxes, fees, and surcharges that disproportionately affect wealthier homeowners, short-term rental operators, and luxury real estate transactions.

The takeaway? Where and how you own and use property may increasingly affect what you pay.

Rhode Island’s “Taylor Swift Tax”

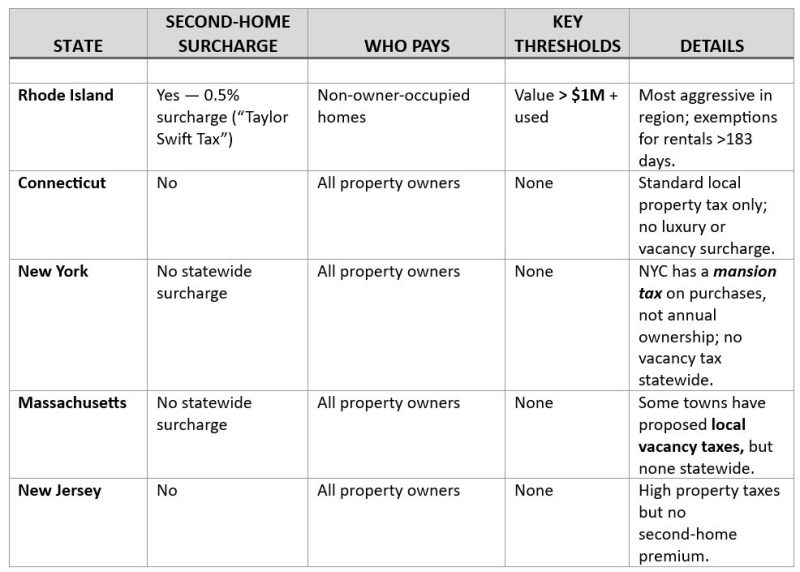

Rhode Island is taking one of the region’s most direct approaches. Beginning July 1, the state will impose a surcharge on certain non-owner-occupied residential properties assessed at $1 million or more.i (The law is commonly referred to as the “Taylor Swift Tax” because of attention surrounding luxury seasonal homes in Rhode Island, including Taylor Swift’s well-known Westerly property, though she has no connection to the legislation itself.)

Rather than taxing the full property value, Rhode Island applies the surcharge only to assessed value above $1 million. The effective rate is roughly 0.5% of that excess value. Properties rented for more than 183 days in the prior year may qualify for an exemption if they comply with rental and tax rules.ii

The policy reflects a broader shift in thinking: states are increasingly targeting expensive homes that sit vacant for much of the year while attempting to encourage fuller occupancy or expanded rental availability.

Massachusetts: High Earners, High-Value Sales, and Short-Term Rentals

Massachusetts has taken a broader approach to taxing wealth. The state’s millionaire surtax imposes an additional 4% tax on annual income above an inflation-adjusted threshold, affecting many high earners, investors, business owners, and taxpayers experiencing significant capital gains.iii

Massachusetts is also increasing oversight of certain high-value real estate sales. Beginning in late 2025, some Massachusetts property transactions of $1 million or more involving nonresident sellers require withholding filings at closing, and withholding may apply depending on the circumstances.iv

At the local level, seasonal communities on Cape Cod are increasingly targeting short-term rentals through occupancy taxes, registration fees, and community impact charges intended to address housing shortages and tourism pressures. Nantucket, for example, adopted a 3% community impact fee on certain non-owner-occupied short-term rentals operated by owners with multiple rental properties.v For owners of vacation homes or income-producing property, these local rules can materially affect carrying costs and profitability.

New York: Luxury Transactions Carry Higher Costs

New York offers a different model. Rather than annual taxes on second homes, New York City imposes a “mansion tax” on high-value residential purchases, increasing transaction costs for luxury buyers. Additional transfer taxes on expensive properties can add meaningfully to acquisition costs at higher price points.vi

The approach differs from Rhode Island’s, but the result is similar: affluent homeowners and luxury buyers shoulder a larger share of housing-related tax revenue.

Connecticut and New Jersey: A Different Strategy

Not every Northeastern state is targeting wealth through new second-home surcharges or rental-related fees. Connecticut and New Jersey, for example, continue to rely more heavily on traditionally high property taxes and broader tax structures rather than special annual taxes on luxury vacation homes.

A Trend Worth Watching

For affluent homeowners, the lesson is an important one: tax exposure can look very different depending on where and how property is owned or used. The key question may no longer be simply, “What are property taxes where I live?” but rather, “How does the way I own and use property affect what I owe?”

Washington Trust Wealth Management Can Help

If you own multiple homes, generate rental income, or anticipate a significant real estate transaction, our experienced wealth advisors can work with you and your tax professional to identify and navigate additional taxes and fees that may be tied to your wealth and property.

i Rhode Island Division of Taxation – Non-Owner Occupied Property Tax

ii Rhode Island Division of Taxation – Non-Owner Occupied Property Tax

iii Mass.gov: Massachusetts 4% Surtax on Taxable Income

iv Mass.gov – Filing and Withholding Rules: Real Estate Sales of $1 Million or More